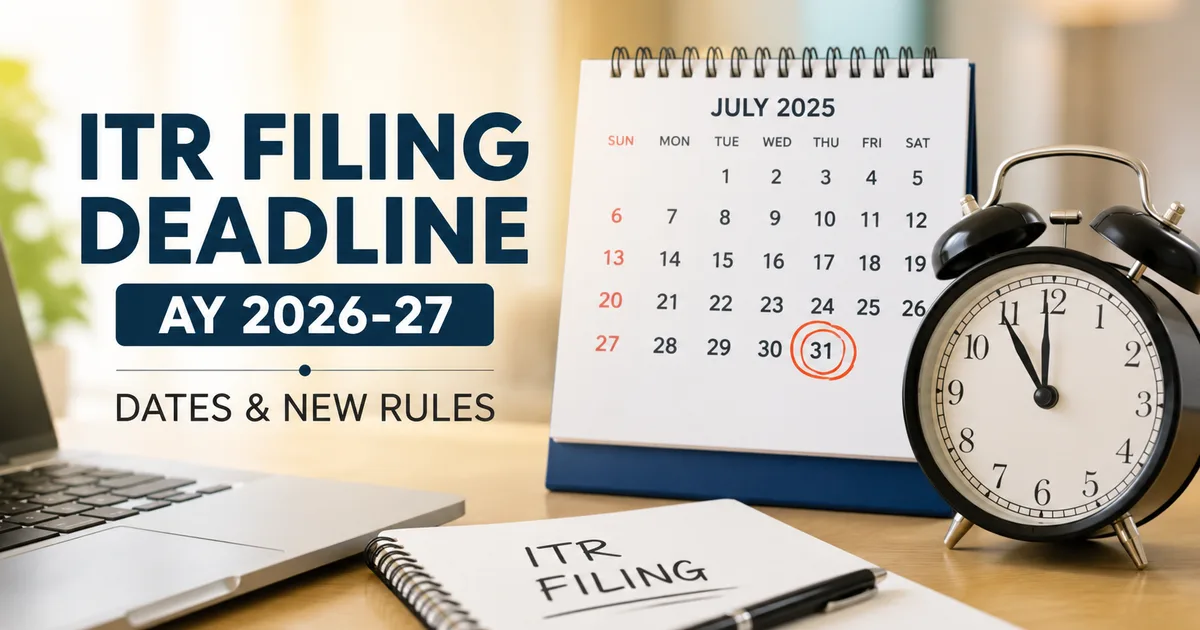

Every middle-class Indian knows the absolute panic of July. You're scrambling to find your Form 16 and asking your CA why your TDS hasn't updated yet. At the same time, you're praying the tax portal doesn't crash. But this year, the government decided to stir the pot a bit. If you're trying to figure out the ITR filing deadline for AY 2026-27, you'll notice things look slightly different. The old system of having one single date for almost everyone's been tweaked. And missing these new dates is going to frustrate you, and it'll cost you real money. Knowing the new rules saves you from unwanted penalties and notices.

Let's get the terminology out of the way first. We're talking about Assessment Year 2026-27. That corresponds to Financial Year 2025-26 (which makes sense, actually). Basically, you're reporting what you earned between April 1, 2025, and March 31, 2026. The tax department calls the year you earned it the Financial Year, and the year you file the Assessment Year. In my experience, this is where people get tripped up. It's a simple distinction. But it confuses everyone. Honestly, it's just jargon, but getting it wrong means you might file the wrong form.

Why the ITR filing last date 2026 is different for some

For years, July 31 was the magic date. If you didn't file by then, you were in trouble. But the tax department noticed that their servers were dying under the weight of millions of last-minute filings. So they split the crowd. If you're a salaried employee or a pensioner, or if you earn money from house property or interest, your due date's still July 31, 2026. That hasn't changed. You'll still need to mark this date on your calendar.

But if you run a business or work as a professional (like a doctor, lawyer, developer, or consultant) and don't need a tax audit, you'll get a bit of breathing room. Your new deadline's August 31, 2026. Honestly, it's a major change. It gives professionals an extra month to sort books and file. I think it's good because it spreads the load. I'm not sure exactly why they split this now, but it helps. If you're a freelancer earning UPI payments, you now have until August's end to get your act together.

This extra month's specifically designed for those filing under presumptive taxation schemes like Section 44AD or Section 44ADA. Under these schemes, you don't have to maintain detailed books of accounts. You just declare a percentage of your gross receipts as profit. For instance, if you're a freelance coder and your total receipts are ₹15 lakh, you can declare 50% of that as profit under Section 44ADA. You'll file ITR-4, and your deadline's August 31.

What if your business needs an audit? The deadline for audit cases remains October 31, 2026. And if you're involved in international transactions that require a transfer pricing report, your date's November 30, 2026. These deadlines are mostly for corporate houses and large partnerships, so if you're an individual running a small shop, you don't need to worry about these late dates.

The staggering of deadlines is a practical move to prevent the online filing portal from crashing, which has been a recurring issue for Indian taxpayers in previous years.

Major changes to income tax return deadlines and rules

Besides the dates, other things've changed too. For one, the government's updated how they process TDS and TCS returns. According to a CAclubindia report on the IT Act 2025 updates, the dates for employers and deductors to file their quarterly returns've become much stricter. Basically, they want to ensure that tax credits reflect on your portal much faster than before.

Why does this matter to you? It matters because you can't file your ITR without your Form 16 or your Annual Information Statement (AIS) being fully updated (which makes sense, actually). If your employer files their TDS return late, the tax you paid won't show up on your tax portal. That means if you try to file early, you might get a tax demand notice because the system thinks you haven't paid enough tax. The whole portal becomes a complete mess.

Let's look at a common example. Suppose you have a fixed deposit at a bank like SBI. The bank deducts TDS on your interest income. They're supposed to upload this data quarterly. If they delay the final quarter's filing, your Form 26AS won't show that tax credit. If you file your return without checking, the tax department'll ask you to pay that tax again, plus interest. You'll then have to file a rectification request later.

So, even if the portal opens in May, don't rush. The Times of India recently advised salaried taxpayers to wait until mid-June to file. In my experience, waiting is always the safer bet. The reason's simple. Employers've until June 15 to issue Form 16. The AIS and Form 26AS also take time to sync. If you file before these documents are ready, you'll end up making mistakes. And mistakes mean notices.

Choosing the correct ITR form's also important. For most individual taxpayers, the choices are ITR-1 (Sahaj) or ITR-4 (Sugam). If you're a salaried person with a total income up to ₹50 lakh, you'll use ITR-1. But if you're a small business owner or professional opting for presumptive taxation, you'll use ITR-4. A Financial Express report notes that ITR-4 has some new fields this year to track bank accounts and cash receipts, so make sure you read the instructions carefully before filling it out. You'll find detailed walk-throughs in our guides section to help you pick the right form.

The penalty for filing late

Missing the deadline has serious financial consequences, and it'll hurt your wallet. Under Section 234F of the Income Tax Act, filing after your due date attracts a mandatory late fee. Look, there's no way around it.

If your total income's more than ₹5 lakh, the late fee's ₹5,000. If your income's ₹5 lakh or less, the fee is ₹1,000. You've to pay this fee before you can even submit your return. There's no escaping it. Even if your net tax liability's zero after deductions, you'll still have to pay the late fee if your gross total income exceeds the basic exemption limit.

But the late fee isn't the only penalty. If you ask me, these penalties are way too harsh for minor mistakes. If you owe tax, you'll also have to pay interest on the unpaid amount. Under Section 234A, interest's charged at 1% per month (the math can get a bit fuzzy, but it's calculated from the day after the due date). So, if you're three months late, that's an extra 3% on your bill. It adds up fast.

There's another major downside to filing late. You lose the right to carry forward certain losses. If you have capital losses from stocks or business losses, you can normally carry them forward to offset future gains. But if you file late, you'll lose this benefit. It's a heavy price to pay for a few days of delay. Also, if you've a tax refund due, the department won't pay you interest on that refund for the period of the delay. That's a double blow to your wallet.

How the revised returns process has changed

Thankfully, the government's extended the timeline for filing a revised return. A revised return's what you file when you discover an error in your original filing. For example, maybe you forgot to declare some interest income or missed claiming a deduction under Section 80C (thank goodness for small mercies).

In the past, you only had until December 31 of the assessment year to file a revised return. If you realized you made a mistake in January, you were out of luck. I'm not sure exactly why it took them so long to make this change, but for AY 2026-27, you've until March 31, 2027 to file a revised or belated return. This gives you a full 12 months.

But there's a catch. While the window's longer, filing late's now more expensive. If you file a revised return after the original nine-month window, which ends on December 31, 2026, you'll have to pay a late fee. According to a Business Today report on the new tax changes, the penalty's ₹5,000 if your total income exceeds ₹5 lakh, and ₹1,000 if it's less.

So, while you've got more time to fix errors, doing it late is going to cost you. I think this extra time is a lifesaver, but that penalty still hurts. It's always better to double-check your filings in July or August rather than waiting until next year. Make sure to check our news section to stay updated on any CBDT announcements about these fees.

What you should do next

Don't wait until the last minute. Start gathering your documents now. You'll need your Aadhaar card, PAN card, bank statements, and investment proofs. If you've got home loans or insurance policies, get those certificates ready too. You can download most of these from your bank's portal or via DigiLocker. In my experience, sorting this out early saves you a lot of late-night coffee and stress.

- Check your AIS and Form 26AS on the income tax portal to ensure all TDS matches.

- Download your Form 16 from your employer's portal once it's available after June 15.

- Confirm your filing category and note down your specific deadline, which is either July 31 or August 31.

- Calculate your total income and check if you'll need to pay any self-assessment tax.

- File your return well before the deadline to avoid portal congestion and late fees.

If you're unsure about your taxes, it's best to consult a professional. If you ask me, doing it on your own when you aren't sure can get a bit sketchy. You'll read more about planning in our explainers section. Taking a few hours now'll save you from a lot of stress, though there's still the task of actually logging in.